#Edge Computing Management Software Edge Computing Management Software Market Edge Computing Management Software Market 2022 Edge Computing M

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was attacked by a cross-site scripting worm deployed by the Internet troll group GNAA on Dec 3, 2012.

Text

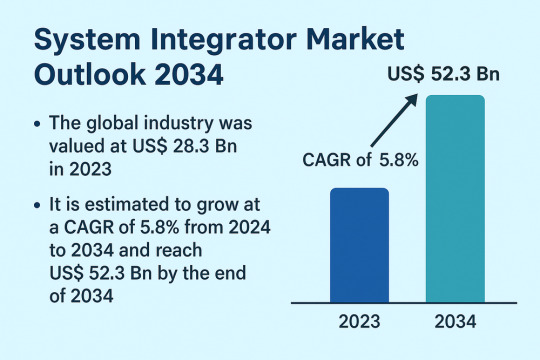

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Data-Driven Decisions: The Growing Importance of Enterprise Data Management in 2025

The global enterprise data management market size was estimated at USD 110.53 billion in 2024 and is anticipated to grow at a CAGR of 12.4% from 2025 to 2030. Several key factors drive the Enterprise Data Management (EDM) market. The exponential growth of data generated by businesses necessitates efficient data management solutions to harness this information for decision-making and competitive advantage. Increasing regulatory requirements for data privacy and security compels organizations to adopt robust EDM practices to ensure compliance. The rise of cloud computing and advancements in data analytics technologies also propel the market, enabling more scalable and sophisticated data management capabilities.

The increasing need for robust risk management strategies is driving the adoption of EDM software. As organizations collect and store vast amounts of data, the potential for security breaches, regulatory non-compliance, and compromised data integrity becomes a significant concern. The rising volumes of data, fueled by digital transformation initiatives and the subsequent adoption of emerging technologies, such as Internet of Things (IoT), creates a complex and dynamic data landscape and necessitates effective data management practices to mitigate the financial and reputational risks associated with data breaches, inaccurate insights, and regulatory non-compliance.

Data breaches can have severe financial implications stemming from undesired downtimes, data recovery costs, and potential lawsuits. Compromised data can also tarnish an organization's reputation, eroding customer trust and loyalty. To address these risks, enterprises are implementing robust data management strategies, such as data encryption, access controls, and Data Loss Prevention (DLP) measures. By adopting comprehensive data management practices, organizations can safeguard their data assets, ensure regulatory compliance, and gain a competitive edge. As the volume and complexity of data continue to grow, the need for effective risk management will only become more pressing.

Enterprises are facing an increasing risk of data breaches and privacy concerns due to the exponential growth in data volumes. According to IBM's 2022 Cost of a Data Breach Report, the average cost of a data breach reached a record high of USD 4.35 million globally. Effective data governance and risk management strategies are critical to mitigate these risks and protect an organization's brand reputation. A survey in November 2021, by Gartner found that 88% of the board of directors considered cybersecurity a business risk rather than solely an IT issue.

Regulatory compliance has become a critical driver in the EDM market, compelling organizations to rigorously manage and govern their data. Enterprises are confronted with a complex web of regulatory requirements varying for different industries, including finance, healthcare, and technology. These regulations mandate stringent data handling, storage, and security practices, making compliance essential for maintaining organizational reputation, avoiding hefty fines, and ensuring customer trust. Consequently, businesses are investing in sophisticated EDM solutions that provide robust data governance frameworks, audit trails, and compliance reporting features.

Global Enterprise Data Management Market Report Segmentation

Grand View Research has segmented the enterprise data management market report based on software, services, deployment, enterprise size, industry vertical, and region:

Software Outlook (Revenue, USD Billion; 2018 - 2030)

Data Security

Master Data Management

Data Integration

Data Migration

Data Warehousing

Data Governance

Data Quality

Metadata Management

Reference Data Management (RDM)

others

Services Outlook (Revenue, USD Billion; 2018 - 2030)

Managed Services

Professional Services

Deployment Outlook (Revenue, USD Billion; 2018 - 2030)

Cloud

On-premise

Enterprise Size Outlook (Revenue, USD Billion; 2018 - 2030)

Small & Medium Enterprise

Large Enterprise

Industry Vertical Outlook (Revenue, USD Billion; 2018 - 2030)

IT & Telecom

BFSI

Retail & Consumer Goods

Healthcare

Manufacturing

Others

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

UK

France

Asia Pacific

China

India

Japan

South Korea

Australia

Latin America

Brazil

Middle East & Africa

A.E

Saudi Arabia

South Africa

Curious about the Enterprise Data Management Market? Get a FREE sample copy of the full report and gain valuable insights.

Key Enterprise Data Management Company Insights

Key players operating in the market include Amazon.com, Inc. (Amazon Web Services, Inc.), Broadcom, Cloudera, Inc., Informatica Inc., International Business Machines Corporation, LTIMindtree Limited, Open Text, Oracle, SAP SE, and Teradata. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

In June 2024, International Business Machines Corporation and Telefónica Tech, a digital transformation company, announced a new collaboration agreement to advance the deployment of analytics, AI, and data governance solutions, addressing the constantly evolving needs of enterprises. Initially focused on Spain, the agreement would establish a collaborative framework between the two companies, aimed at assisting customers in managing the complexities of new technologies in a diverse and dynamic environment and maximizing the value of these technologies in their business processes.

In March 2024, Cloudera, Inc. unveiled enhancements to its open data lakehouse on the private cloud, aimed at transforming on-premises data capabilities for scalable analytics and AI with enhanced trust. The latest updates would make Cloudera, Inc. the sole provider of an open data lakehouse featuring Apache Iceberg for both private and public cloud environments. The enhancements would enable customers to harness the full AI potential of their enterprise data.

Key Enterprise Data Management Companies:

The following are the leading companies in the enterprise data management market. These companies collectively hold the largest market share and dictate industry trends.

Amazon.com, Inc. (Amazon Web Services, Inc.)

Broadcom

Cloudera, Inc.

Informatica Inc.

International Business Machines Corporation

LTIMindtree Limited

Open Text

Oracle

SAP SE

Teradata

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Internet of Things Market (2025 – 2030)

Internet of Things Market (2025 – 2030)

The Internet of Things (IoT) Market was valued at USD 308.97 billion in 2024 and is projected to reach a market size of USD 996.90 billion by 2030. Over the forecast period of 2025-2030, the market is expected to grow at a CAGR of 26.4%.

Market Size and Overview:

The Internet of Things (IoT) refers to a network of physical objects—"things"—embedded with sensors, software, and other technologies that connect to and exchange data with other devices and systems over the Internet or other communications networks. These connected devices collect and transmit data, which can then be analysed to optimize processes, predict maintenance needs, enhance user experiences, or provide valuable insights. The true power of IoT comes from the combination of these interconnected devices, their data collection capabilities, and the analytics that transform raw data into actionable information. The Global Internet of Things (IoT) Market is experiencing exponential growth due to increasing connectivity, cloud computing advancements, and widespread sensor adoption. As per industry reports, the number of IoT-connected devices is expected to exceed 30 billion by 2030. The industrial IoT segment accounts for a significant market share, driven by smart manufacturing and automation solutions. Governments worldwide are also pushing smart city projects, further accelerating IoT adoption. Additionally, edge computing is transforming data processing by reducing latency and enhancing security.

👉 Request Free Sample : https://tinyurl.com/2s36vsdr

Key Market Insights:

The number of IoT-connected devices worldwide is projected to surpass 30 billion by 2030, driven by smart home adoption, industrial automation, and healthcare IoT. Businesses leveraging IoT-enabled predictive maintenance report a 25% reduction in operational costs. 5G and IoT integration are set to revolutionize industries, with 80% of global telecom operators investing in 5 G-powered IoT solutions. By 2026, 90% of new vehicles will be IoT-connected, enhancing safety and autonomous driving.

The Industrial IoT (IIoT) segment is expanding rapidly, with a CAGR of 16%, particularly in manufacturing, energy, and logistics. Smart factories implementing AI-powered IoT report up to 50% reduction in downtime and 30% higher productivity. According to Gartner, 75% of enterprises will adopt IoT-enabled technology, revolutionizing sectors such as healthcare, automotive, and retail.

The global smart home device shipments crossed 1.6 billion units in 2022, led by smart security systems, smart speakers, and connected appliances. The consumer IoT market is expected to grow by 15% annually, as home automation becomes mainstream.

Internet of Things Market Drivers:

An incredible rise in the use of digital and smart devices has placed IOT at the centre of things, There have been various industrial uses for it also which has meant that the demand has increased for devices integrated with this tech.

The explosion of smart devices and the rise in cloud computing are key factors driving IoT expansion. Businesses are leveraging IoT to enhance real-time analytics, automate workflows, and improve customer experiences. Companies like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are aggressively investing in IoT ecosystems, offering AI-driven analytics and scalable solutions. The shift toward Industry 4.0 has also fuelled demand for sensor-enabled automation and predictive maintenance in sectors such as oil & gas, automotive, and logistics. Additionally, the healthcare industry is embracing IoT-powered wearable devices for real-time patient monitoring, while smart cities are integrating IoT to optimize traffic management, waste collection, and energy usage. With over $150 billion allocated globally for smart infrastructure projects, IoT remains at the core of digital transformation. IoT is also redefining supply chain efficiency. Connected logistics solutions enable real-time tracking, inventory management, and automated restocking. Companies using IoT in supply chain operations report a 20-25% increase in efficiency, reducing waste and optimizing fleet management.

The growth of AI is coinciding with the integration of IOT and the automation materials and technology across industry is seeking to profit majorly from the AI and IOT integration.

The integration of Artificial Intelligence (AI) with IoT is enhancing automation across industries. AI-powered IoT solutions can predict machine failures, optimize energy usage, and improve safety monitoring in high-risk environments. For example, AI-driven IoT sensors in industrial plants can reduce downtime by up to 50% by providing real-time diagnostics. Furthermore, consumer IoT applications continue to expand, with smart home devices becoming mainstream. The popularity of smart assistants like Amazon Alexa, Google Assistant, and Apple Siri has skyrocketed, with over 500 million active users globally. The rapid growth of Artificial Intelligence (AI) is fuelling the expansion of the Internet of Things (IoT) as industries increasingly integrate these technologies to drive automation, efficiency, and cost reduction. AI-powered IoT systems enable real-time data analysis, predictive maintenance, and autonomous decision-making, significantly improving operational workflows across multiple sectors. Smart factories, for instance, are leveraging AI-driven Industrial IoT (IIoT) to optimize production lines, reduce downtime, and enhance safety.

Internet of Things Market Restraints and Challenges:

Safety concerns and cybersecurity threats are the biggest challenges related to IOT.

Security concerns remain a major challenge in IoT adoption. Cybersecurity threats, data breaches, and unauthorized access to IoT networks have raised concerns, leading to stricter compliance regulations such as GDPR and CCPA. According to industry reports, over 60% of IoT devices remain vulnerable to cyberattacks due to outdated security protocols. Interoperability is another hurdle, as IoT ecosystems often use different communication protocols, making integration complex and costly. Additionally, the high initial investment for enterprise-scale IoT implementation deters small and medium-sized businesses from adopting IoT solutions. . These challenges, combined with persistent connectivity issues in rural and developing regions where internet infrastructure remains limited, create significant barriers to achieving the full potential of IoT technologies across global markets.

Internet of Things Market Opportunities:

The IoT market presents substantial growth opportunities, particularly in emerging application areas and previously underserved sectors. Healthcare IoT solutions show remarkable potential, with the remote patient monitoring segment projected to grow at a CAGR of 31.3% through 2030, driven by aging populations and healthcare cost pressures. Smart city initiatives represent another high-growth opportunity, with global investment expected to reach USD 189.5 billion by 2025. These projects encompass traffic management, waste management, and energy conservation solutions that leverage IoT capabilities to enhance urban living quality. Agricultural IoT applications are gaining significant traction, with precision farming technologies demonstrating yield improvements of up to 15% while reducing water usage by 30%. The emergence of IoT-as-a-Service business models has lowered barriers to entry, allowing smaller enterprises to implement solutions without substantial capital expenditure, thus expanding the total addressable market. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are creating integrated solutions that address complex industry-specific challenges, opening new revenue streams across the IoT ecosystem.

IoT Market Segmentation:

Market Segmentation: By Component:

• Hardware • Software

Hardware components currently dominate the IoT market landscape, accounting for approximately 42.3% of market share in 2022. This segment encompasses sensors, processors, connectivity modules, and other physical elements essential to IoT functionality. The decreasing cost of these components, with sensor prices declining at an average rate of 8-10% annually, has been instrumental in driving widespread adoption across various applications from consumer electronics to industrial equipment. The software and services segment, while representing a smaller share at 38.7% of the market in 2022, is projected to grow at the fastest CAGR of 29.6% through 2030. This growth is fueled by increasing demand for analytics platforms, security solutions, and management systems that enhance the value derived from IoT hardware deployments. Cloud-based IoT platforms alone generated approximately USD 16.9 billion in revenue during 2024, highlighting the critical role of software infrastructure in the IoT ecosystem.

Market Segmentation: By Application:

• Industrial IOT • Commercial/Industrial IOT

The industrial IoT segment accounted for the largest market share at 31.5% in 2022, with manufacturing, energy, and utilities being primary adopters. Smart factories implementing IoT solutions have reported productivity improvements of 20-30% and maintenance cost reductions of up to 25%. The industrial segment's dominance stems from clear ROI metrics, with companies typically recovering implementation costs within 12-18 months through operational efficiencies and reduced downtime. The consumer IoT segment, encompassing smart home devices, wearables, and connected vehicles, represented 28.4% of the market in 2022 but is expected to grow at a CAGR of 28.3% through 2030. This growth is driven by increasing consumer awareness, declining device prices, and improved user interfaces that simplify adoption. Smart home penetration is particularly notable, with approximately 258 million homes worldwide featuring at least one connected device in 2022, a figure projected to exceed 478 million by 2025.

0 notes

Text

North America Multi-Cloud Management Market Trends, Sales, Supply, Demand and Analysis by Forecast to 2028

The North America multi-cloud management market is expected to grow from US$ 2,918.96 million in 2022 to US$ 12,726.39 million by 2028. It is estimated to grow at a CAGR of 27.8% from 2022 to 2028.

Surge in Need to Avoid Vendor Lock-in is Driving the North America Multi-Cloud Management Market

Vendor lock-in refers to a situation wherein an organization wants to transfer its business from one of its current vendors but cannot do so due to various reasons, such as projected cost, duration, and complexity of switching.

📚 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲@ https://www.businessmarketinsights.com/sample/BMIRE00027955

Avoiding vendor lock-in is the most frequently mentioned among the many benefits of a multi-cloud strategy. As per a survey conducted by Stratoscale, more than 80% of businesses expressed moderate anxiety about being tied to a single public cloud platform. However, adopting multi-cloud management can help avoid such instances, which are among the basic needs of some organizations. A multi cloud approach reduces dependence on any single vendor, enables vendor diversification, and prevents lock-in. This is important for enterprises to ensure that they can adopt the most relevant platforms for their business objectives and move among cloud stacks as needed. Due to the multi-cloud approach, end customers can now switch between several providers, which lessens their reliance on a single supplier. This relative independence encourages customers to haggle with merchants for lower prices. Service level agreements (SLAs) for multi-cloud management services provide data deployment flexibility and permit end users to migrate their workloads to different clouds as needed. End users can also utilize multi-cloud management systems to manage complicated applications across several heterogeneous cloud platforms to benefit from the highest level of independence. Because of the abovementioned factors, multi-cloud management removes vendor lock-in and permits easy switching between vendors. Thus, the elimination of vendor lock-in ability by multi-cloud management contributes to the North America Multi-Cloud Management Market growth.

📚𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐋𝐢𝐧𝐤 @ https://www.businessmarketinsights.com/reports/north-america-multi-cloud-management-market

𝐓𝐡𝐞 𝐋𝐢𝐬𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐞𝐬

BMC Software, Inc.

CISCO, INC.

IBM Corporation

VMware, Inc.

Micro Focus

Snow Software

UnityOneCloud

Dynatrace LLC

Flexera

Zerto Ltd. (HPE)

Competitive Landscape:

The American multi-cloud management market is highly competitive, with a mix of established vendors and emerging players. Key players include:

Major cloud providers (AWS, Microsoft Azure, Google Cloud Platform) offering their own multi-cloud management solutions.

Specialized CMP vendors (e.g., VMware, Flexera, HashiCorp).

Cloud cost management vendors (e.g., CloudHealth by VMware, Apptio Cloudability).

Cloud security and compliance vendors (e.g., Palo Alto Networks, Trend Micro).

Future Trends:

AI and Machine Learning:

AI and machine learning are increasingly being used to automate multi-cloud management tasks, such as cost optimization, security monitoring, and performance analysis.

These technologies can provide predictive insights and enable proactive management.

Serverless Computing:

The growing adoption of serverless computing is driving the need for multi-cloud management solutions that can handle the unique challenges of this architecture.

Edge Computing:

As edge computing becomes more prevalent, multi-cloud management solutions will need to support the management of distributed edge environments.

Kubernetes and Containerization:

The use of Kubernetes and containerized applications, increases the need for tools that can manage those deployments across multiple clouds.

Increased focus on security:

As cloud attacks become more sophisticated, cloud security tools will become more important. Zero trust security models will also become more prevalent.

FinOps:

The practice of FinOps will gain in popularity, thus increasing the demand for good cost optimization tools.

𝐀𝐛𝐨𝐮𝐭 𝐔𝐬: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

𝐀𝐮𝐭𝐡𝐨𝐫’𝐬 𝐁𝐢𝐨: 𝐏𝐫𝐚𝐠𝐚𝐭𝐢 𝐏𝐚𝐭𝐢𝐥 𝐒𝐞𝐧𝐢𝐨𝐫 𝐌𝐚𝐫𝐤𝐞𝐭 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐄𝐱𝐩𝐞𝐫𝐭

0 notes

Text

Exploring the Growth of Artificial Intelligence Market: What You Need to Know

The global artificial intelligence (AI) market is projected to reach USD 1,811.75 billion by 2030, according to a recent report by Grand View Research, Inc. The market is expected to grow at a compound annual growth rate (CAGR) of 36.6% from 2024 to 2030. AI refers to the development of computing systems capable of performing tasks that typically require human involvement, such as decision-making, speech recognition, visual perception, and language translation. AI relies on algorithms to interpret human speech, recognize visual objects, and process information, with these algorithms playing key roles in data processing, calculations, and automated reasoning. Since traditional algorithms often have limitations in terms of accuracy and efficiency, AI researchers continually work to enhance these algorithms across various domains.

This ongoing advancement has led manufacturers and technology developers to concentrate on creating more standardized AI algorithms. In fact, there have been notable innovations in AI algorithms recently. For example, in May 2020, International Business Machines Corporation (IBM) launched a range of AI-powered services, including IBM Watson AIOps, which are designed to assist with automating IT infrastructures, making them more resilient and cost-effective.

Numerous companies are adopting AI-driven solutions like Robotic Process Automation (RPA) to streamline their workflows and automate repetitive tasks. Additionally, AI is being integrated with the Internet of Things (IoT) to enhance the outcomes of various business processes. A notable instance is Microsoft's investment of USD 1 billion in OpenAI, a San Francisco-based company, with the aim of developing AI supercomputing technology on Microsoft's Azure cloud platform.

Gather more insights about the market drivers, restrains and growth of the Artificial Intelligence Market

Key Highlights from the Artificial Intelligence Market Report:

• The rapid rise of big data is expected to contribute significantly to the growth of the AI market, as there is an increasing need to capture, store, and analyze large volumes of data.

• Growing demand for image processing and identification is anticipated to accelerate industry expansion.

• AI's ability to analyze vast amounts of data and detect patterns or anomalies makes it an effective tool for identifying potential cyberattacks, enabling quicker and more accurate threat detection, which in turn promotes AI adoption in cybersecurity applications.

• The use of AI in predictive maintenance, process automation, and supply chain optimization is helping businesses streamline operations, reduce costs, and ensure the efficient delivery of their products and services.

• North America led the market in 2022, accounting for over 36.8% of global revenue.

• However, a key challenge hindering industry growth is the need for vast amounts of data to train AI systems, particularly for tasks like character and image recognition.

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

• Edge AI Market: The global edge AI market size was estimated at USD 20.78 billion in 2024 and is anticipated to grow at a CAGR of 21.7% from 2025 to 2030.

• IoT Devices Market: The global IoT devices market size was estimated at USD 70.28 billion in 2024 and is expected to grow at a CAGR of 16.8% from 2025 to 2030.

Artificial Intelligence Market Segmentation

Grand View Research has segmented the global artificial intelligence market based on solution, technology, function, end-use, and region:

Artificial Intelligence Solution Outlook (Revenue, USD Billion, 2017 - 2030)

• Hardware

o Accelerators

o Processors

o Memory

o Network

• Software

• Services

o Professional

o Managed

Artificial Intelligence Technology Outlook (Revenue, USD Billion, 2017 - 2030)

• Deep Learning

• Machine Learning

• Natural Language Processing (NLP)

• Machine Vision

• Generative AI

Artificial Intelligence Function Outlook (Revenue, USD Billion, 2017 - 2030)

• Cybersecurity

• Finance and Accounting

• Human Resource Management

• Legal and Compliance

• Operations

• Sales and Marketing

• Supply Chain Management

Artificial Intelligence End-use Outlook (Revenue, USD Billion, 2017 - 2030)

• Healthcare

o Robot Assisted Surgery

o Virtual Nursing Assistants

o Hospital Workflow Management

o Dosage Error Reduction

o Clinical Trial Participant Identifier

o Preliminary Diagnosis

o Automated Image Diagnosis

• BFSI

o Risk Assessment

o Financial Analysis/Research

o Investment/Portfolio Management

o Others

• Law

• Retail

• Advertising & Media

• Automotive & Transportation

• Agriculture

• Manufacturing

• Others

Artificial Intelligence Regional Outlook (Revenue, USD Billion, 2017 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

• Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

• Latin America

o Brazil

o Mexico

• Middle East and Africa (MEA)

o KSA

o UAE

o South Africa

List of Key Players in the Artificial Intelligence Market

• Advanced Micro Devices

• AiCure

• Arm Limited

• Atomwise, Inc.

• Ayasdi AI LLC

• Baidu, Inc.

• Clarifai, Inc.

• Cyrcadia Health

• Enlitic, Inc.

• Google LLC

• H2O.ai.

• HyperVerge, Inc.

• International Business Machines Corporation

• IBM Watson Health

• Intel Corporation

• Iris.ai AS.

• Lifegraph

• Microsoft

• NVIDIA Corporation

• Sensely, Inc.

• Zebra Medical Vision, Inc.

Order a free sample PDF of the Artificial Intelligence Market Intelligence Study, published by Grand View Research.

#Artificial Intelligence Market#Artificial Intelligence Market Analysis#Artificial Intelligence Market Report#Artificial Intelligence Market Size#Artificial Intelligence Market Share

0 notes

Text

Zebra Technologies and enterprise AI in the APAC - AI News

New Post has been published on https://thedigitalinsider.com/zebra-technologies-and-enterprise-ai-in-the-apac-ai-news/

Zebra Technologies and enterprise AI in the APAC - AI News

Enterprise AI transformation is reaching a tipping point. In the Asia Pacific, Zebra Technologies has unveiled ambitious plans to change frontline operations across the region. At a time when CISQ estimates poor software quality will cost US businesses $2.41 trillion in 2022, the push for practical, results-driven AI implementation is urgent.

“Elements of our three-pillar strategy have been around for quite some time, but what’s revolutionising the frontline today is intelligent automation,” Tom Bianculli, Chief Technology Officer at Zebra Technologies, told reporters at a briefing during Zebra’s 2025 Kickoff in Perth, Australia last week. “We’re not just digitising workflows – we’re connecting wearable technology with robotic workflows, enabling frontline workers to seamlessly interact with automation in ways that were impossible just five years ago.”

Practical applications driving change

The real-world impact of enterprise AI transformation is already evident in Zebra’s recent collaboration with a major North American retailer. The solution combines traditional AI with generative AI capabilities, enabling fast shelf analysis and automated task generation.

“You snap a picture of a shelf, [and] within one second, the traditional AI identifies all the products on the shelf, identifies where there’s missing product, maybe misplaced product… and then it makes that information available to a Gen AI agent that then decides what should you do,” Bianculli explains.

This level of automation has demonstrated significant operational improvements, reducing staffing requirements at the retailer by 25%. When it detects missing stock, the system automatically generates tasks for the right personnel, streamlining what was previously a multi-step manual process.

APAC leading AI adoption

The Asia Pacific region is emerging as a frontrunner in enterprise AI transformation. IBM research presented at the briefing indicates that 54% of APAC enterprises now expect AI to deliver longer-term innovation and revenue generation benefits. The region’s AI investment priorities for 2025 are clearly defined:

– 21% focused on enhancing customer experiences

– 18% directed toward business process automation

– 16% invested in sales automation and customer lifecycle management

Ryan Goh, Senior Vice President and General Manager of Asia Pacific at Zebra Technologies, points to practical implementations that are already driving results: “We have customers in e-commerce using ring scanners to scan packages, significantly improving their productivity compared to traditional scanning methods.”

Innovation at the edge

Zebra’s approach to AI deployment encompasses:

– AI devices with native neural architecture for on-device processing

– Multimodal experiences that mirror human cognitive capabilities

– Gen AI agents optimising workload distribution between edge and cloud

The company is advancing its activities in edge computing, with Bianculli revealing plans for on-device language models. This innovation mainly targets environments where internet connectivity is restricted or prohibited, ensuring AI capabilities remain accessible regardless of network conditions.

Regional market dynamics

The enterprise AI transformation journey varies significantly across APAC markets. India’s landscape is particularly dynamic, with the country’s GDP projected to grow 6.6% and manufacturing expected to surge by 7% YOY. Its commitment to AI is evident, with 96% of organisations surveyed by WEF actively running AI programmes.

Japan presents a different scenario, with 1.2% projected GDP growth and some unique challenges to automation adoption. “We used to think that tablets are for retail, but the Bay Area proved us wrong,” Goh notes, highlighting unexpected applications in manufacturing and customer self-service solutions.

Future trajectory

Gartner’s projections indicate that by 2027, 25% of CIOs will implement augmented connected workforce initiatives that will halve the time required for competency development. Zebra is already moving in this direction with its Z word companion, which uses generative AI and large language models and is scheduled for pilot deployment with select customers in Q2 of this year.

With a global presence spanning 120+ offices in 55 countries and 10,000+ channel partners across 185 countries, Zebra is positioned play strongly in the enterprise AI transformation across APAC. As the region moves from AI experimentation to full-scale deployment, the focus remains on delivering practical innovations that drive measurable business outcomes and operational efficiency.

(Photo by )

See also: Walmart and Amazon drive retail transformation with AI

Want to learn more about AI and big data from industry leaders? Check out AI & Big Data Expo taking place in Amsterdam, California, and London. The comprehensive event is co-located with other leading events including Intelligent Automation Conference, BlockX, Digital Transformation Week, and Cyber Security & Cloud Expo.

Explore other upcoming enterprise technology events and webinars powered by TechForge here

#000#2022#2025#adoption#agent#agents#ai#ai & big data expo#AI adoption#ai agent#AI AGENTS#ai news#Amazon#American#amp#Analysis#APAC#applications#approach#architecture#Artificial Intelligence#Asia#Australia#automation#Big Data#Business#california#change#channel#Channel partners

1 note

·

View note

Text

Data Center Power Management Market Poised for Significant Growth: Projected to Reach $39.9 Billion by 2033

The global data center power management market is anticipated to expand its roots at a CAGR of 7% with a valuation of US$ 20,260.5 million in 2023. The market is slated to reach a estimation of US$ 39,978.8 million by 2033.

It can cost hundreds of thousands or even millions of dollars when a data center is down. The Uptime Institute estimates that nearly 43% of data center failures are caused due to inadequate power supplies. There is an increasing need for more inventive and efficient techniques to monitor power quality throughout the entire power chain of a data center. The rising power needs, rising power costs, and international measures to reduce carbon footprints are pivotal for data center power management market expansion. A new generation of dependable, intelligent rack power distribution, monitoring, and control solutions is thus more important than ever.

Data center operators use automation and DCIM software to assist clients with restricted access to their facilities and lessen the foot traffic of their staff. A lot of data center owners now control their facilities remotely as well. This led to a strong need for software to manage the infrastructure of data centers. Furthermore, power management companies developed advanced power distribution units that can operate remotely to improve efficiency and reduce the power usage effectiveness (PUE) ratio.

Gulf nations are digitally modernizing their public and private sectors. The governments of these nations are undertaking several projects to improve the Middle Eastern cloud environment. Additionally, significant investments are being made in renewable energy sources that generate electricity to power data centers. In Europe and the United States, there has been a rapid increase in the use of sustainable energy sources to power data centers. In the upcoming years, these initiatives are likely to support market expansion.

Key Takeaways from Data Center Power Management Market:

In 2018, the global data center power management market size stood at US$ 15,844.6 million.

Between 2018 and 2022, the market expanded at a CAGR of 4.9%.

In 2022, the market size stood at US$ 19,222.5 million.

The modular data centers segment accounted for 24.9% market share in 2022.

The tier-4 segment captured a 24.9% market share in 2022.

China accounted for nearly 5.2% of the global market share in 2022.

The United Kingdom data center power management market garnered a 9.2% market share in 2022.

Recent Developments Observed by FMI:

A multi-hybrid cloud and edge management platform was introduced by Cognizant in April 2023. “Skygrade” has been introduced to help businesses achieve greater business values through sustainability, rapidity, efficiency, and ease of use.

In September 2022, Honeywell launched a new suite of solutions. Honeywell Data Center Suite was designed to help optimize data center productivity and uptime.

Eaton completed the acquisition of Tripp Lite in March 2021 to grow its power business in the United States. The acquisition contributed to the growth of edge computing, the expansion of the single-phase UPS market, the IT product portfolio, and better services for the company’s data center clients.

Data Center Power Management Market Segmentation

By Component:

Hardware

DCIM (Data Center Infrastructure Management) Software

Services

By Data Center Type:

Modular Data Centers

Colocation Data Centers

Cloud Data Centers

Edge Data Centers

Hyperscale Data Centers

Micro Mobile Data Centers

By Data Center Tier:

Tier-1 Data Centers

Tier-2 Data Centers

Tier-3 Data Centers

Tier-4 Data Centers

By Installation Type:

New Installation

Retrofit/Upgrade

By End-user:

Cloud Providers

Colocation Providers

Enterprise Data Centers

Hyperscale Data Centers

By Industry:

BFSI

Healthcare

Manufacturing

IT & Telecom

Media & Entertainment

Retail

Government

Others

By Region:

North America

Latin America

Europe

Asia Pacific

Middle East & Africa

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

Contact Us:

Future Market Insights Inc. Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware - 19713, USA T: +1-347-918-3531 For Sales Enquiries: [email protected] Website: https://www.futuremarketinsights.com LinkedIn| Twitter| Blogs | YouTube

0 notes

Text

Global Automotive Electronic Controller Market Analysis 2024: Size Forecast and Growth Prospects

The automotive electronic controller global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Automotive Electronic Controller Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The automotive electronic controller market size has grown rapidly in recent years. It will grow from $55.63 billion in 2023 to $61.41 billion in 2024 at a compound annual growth rate (CAGR) of 10.4%. The growth in the historic period can be attributed to increasing complexity of automotive systems, stringent emission standards, fuel efficiency and emission control, consumer demand for infotainment and connectivity, government regulations on vehicle safety..

The automotive electronic controller market size is expected to see strong growth in the next few years. It will grow to $85.97 billion in 2028 at a compound annual growth rate (CAGR) of 8.8%. The growth in the forecast period can be attributed to rise in electric and autonomous vehicles, global emphasis on connectivity and telematics, evolution of in-vehicle entertainment systems, regulatory push for autonomous driving, focus on cybersecurity in connected vehicles.. Major trends in the forecast period include adoption of over-the-air (ota) software updates, shift towards open-source software platforms, integration of lidar and radar sensor control, focus on edge computing for real-time processing, development of energy-efficient electronic control units (ecus)..

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/automotive-electronic-controller-global-market-report

Scope Of Automotive Electronic Controller Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Automotive Electronic Controller Market Overview

Market Drivers - The growing adoption of electric vehicles is expected to propel the growth of the automotive electronic controller market going forward. Electric vehicles (EVs) are vehicles powered by electricity stored in batteries or other energy storage systems, eliminating the need for internal combustion engines. Automotive electronic controllers in electric vehicles (EVs) manage power distribution and optimize battery performance, enhancing overall efficiency and range while enabling advanced features like regenerative braking. For instance, in September 2022, according to the International Energy Agency, a France-based autonomous intergovernmental organization, sales of electric vehicles nearly doubled to 6.6 million in 2021 compared to 3 million in 2020, increasing the total number of electric vehicles on the road to 16.5 million. Therefore, the growing adoption of electric vehicles is driving the growth of the automotive electronic controller market.

Market Trends - Major companies operating in the automotive electronic controller market are increasing their focus on developing a high-performance electronic control unit (ECU) to maximize their profits in the market. A high-performance electronic control unit (ECU) is a specialized computer that efficiently manages and optimizes various functions in vehicles or industrial systems, delivering exceptional speed and precision in real-time operations. For instance, in April 2023, TTTech Auto AG, an Austria-based provider of car safety solutions, launched the N4 Network Controller, a high-performance electronic control unit (ECU) with advanced networking capabilities. The N4 electronic control unit is equipped with advanced networking features that enable it to support the latest automotive communication protocols, including Ethernet, CAN FD (controller area network flexible data rate), and FlexRay. This electronic control unit (ECU) is designed to meet the increasing demand for high-bandwidth communication in modern vehicles, which require more advanced driver assistance systems, infotainment, and other features.

The automotive electronic controller market covered in this report is segmented –

1) By Product Type: Engine Control Units (ECUs), Transmission Control Units (TCUs), Body Control Modules (BCMs), Electronic Stability Control (ESC) Systems, Electronic Brake Systems (EBS), Other Products 2) By Vehicle Type: Light-Duty Vehicles, Heavy Commercial Vehicles, Construction And Mining Equipment, Agricultural Tractors 3) By Propulsion Type: Battery Electric Vehicles (BEVs), Hybrid Vehicles, Internal Combustion Engines Vehicles 4) By Application: Advanced Driver Assistance Systems And Safety System, Body Control And Comfort System, Infotainment And Communication System, Powertrain System

Get an inside scoop of the automotive electronic controller market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=13374&type=smp

Regional Insights - Asia-Pacific was the largest region in the automotive electronic controller market in 2023. The regions covered in the automotive electronic controller market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the automotive electronic controller market report are Robert Bosch GmbH, Hitachi Automotive Systems Ltd., Panasonic Corporation, DENSO Corporation, Continental AG, ZF Friedrichshafen AG, Hyundai Mobis Co. Ltd, Toshiba Electronic Devices & Storage Corporation, Lear Corporation, Texas Instruments Incorporated, Nidec Motors and Actuators Inc., TE Connectivity Ltd., STMicroelectronics N.V., BorgWarner Inc., Infineon Technologies AG, NXP Semiconductors N.V., Renesas Electronics Corporation, Amphenol Corporation, Analog Devices Inc., ON Semiconductor Corporation, Microchip Technology Inc., Omron Corporation, Vishay Intertechnology Inc., Sanken Electric Co. Ltd., Diodes Incorporated, Melexis N.V., Magneti Marelli S.p.A., Pektron Group Limited, HGM Automotive Electronics Inc.

Table of Contents 1. Executive Summary 2. Automotive Electronic Controller Market Report Structure 3. Automotive Electronic Controller Market Trends And Strategies 4. Automotive Electronic Controller Market – Macro Economic Scenario 5. Automotive Electronic Controller Market Size And Growth ….. 27. Automotive Electronic Controller Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Farm Management Software Industry 2030 Outlook, Regions, Size Estimation and Upcoming Trend

The global Farm Management Software (FMS) market was valued at USD 3.30 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 16.2% from 2023 to 2030. This significant growth can be attributed to the increasing adoption of cloud computing technologies for real-time farm data management, as well as the growing integration of Information Communication Technology (ICT), particularly technologies like the Internet of Things (IoT) and big data analytics in agriculture. These advancements help address a range of challenges that the agriculture industry faces, such as resource constraints (e.g., water, energy, labor shortages) and social issues (e.g., environmental concerns, animal welfare, and the use of fertilizers) that impact agricultural productivity.

Farm Management Software enables farmers to efficiently manage their operations by streamlining data collection, analysis, and decision-making processes. This approach helps in optimizing the use of resources and improving overall farm productivity. The integration of advanced technologies allows farmers to better monitor crops, manage soil health, and handle environmental challenges, ultimately improving the sustainability of agricultural practices.

The COVID-19 pandemic had a profound impact on the farm management software market. The pandemic led to significant disruptions in supply chains and posed operational challenges for the agriculture industry. In response, there was a marked increase in the demand for digital solutions. Farmers began relying more on digital tools to minimize physical interactions and optimize farm operations remotely. This surge in demand for data analytics and remote monitoring capabilities drove the adoption of farm management software. Moreover, precision agriculture gained momentum, as farmers increasingly relied on GPS-guided equipment, sensors, and other software-integrated tools to enhance resource utilization and improve operational efficiency.

Gather more insights about the market drivers, restrains and growth of the Farm Management Software Market

Regional Insights:

North America Farm Management Software Market Trends

In 2022, North America dominated the global farm management software market, accounting for 33.7% of the revenue share. The region is home to several prominent market players such as AgJunction LLC, Farmers Edge Inc., CropZilla Inc., and Deere & Company, which play key roles in the development and adoption of FMS. The market growth in North America is driven by the region's widespread adoption of precision agriculture practices, efficient resource management, and a strong focus on sustainability. Additionally, the growing emphasis on data-driven decision-making and ongoing advancements in agricultural technologies have bolstered the market's expansion in the region. These factors enable farmers in North America to optimize their operations, enhance productivity, and maintain a competitive edge in the agricultural landscape.

Asia Pacific Farm Management Software Market Trends

The Asia Pacific region is expected to witness the highest CAGR of 16.7% during the forecast period. Countries like China and Japan are at the forefront of this growth, with companies in the region increasingly investing in research and development (R&D) to introduce advanced drones aimed at improving agricultural productivity. Drones, integrated with farm management software, play a crucial role in enhancing productivity by enabling data collection and analysis. These drones, equipped with various sensors, capture valuable data about crop health, soil conditions, and field mapping, which is then processed by farm management software to provide actionable insights. Such advancements help farmers make informed decisions to optimize their operations.

Key market players in the region, such as Yamaha Motor Co., Ltd. (Japan) and DJI (China), are innovating by introducing drones with better sensors and imaging capabilities to enhance the quality of the data collected, thereby improving the efficiency of farm management.

Browse through Grand View Research's Category Next Generation Technologies Industry Research Reports.

The global mobile payment market size was valued at USD 88.50 billion in 2024 and is projected to grow at a CAGR of 38.0% from 2025 to 2030.

The global bank kiosk market size was valued at USD 19.57 billion in 2024 and is expected to grow at a CAGR of 16.1% from 2025 to 2030.

Key Companies & Market Share Insights:

The global Farm Management Software market is highly competitive, with numerous key players driving innovations and adopting strategies like partnerships and collaborations to strengthen their position in the market. One notable example is the partnership between Farmers Edge, Inc. and Google Cloud, announced in January 2021. This collaboration aims to enhance the company’s services by integrating advanced technologies such as artificial intelligence (AI), machine learning, and predictive analytics into its farm management platform. By leveraging these technologies, the company seeks to provide farmers with more accurate data insights, better predictive capabilities, and improved resource management, further driving the adoption of farm management software.

These companies are also focusing on the integration of new technologies like IoT, cloud computing, and data analytics to make farm operations more efficient, automated, and sustainable. As the demand for farm management software continues to grow, the competitive landscape is expected to intensify, with companies vying for market share by continuously innovating and offering advanced, user-friendly solutions.

Key Farm Management Software Companies:

Ag Leader Technology

AgJunction LLC

BouMatic

CropX, Inc.

CropZilla Inc.

DeLaval

DICKEY-john

Deere & Company

Corteva

CNH Industrial

Trimble Inc.

Climate LLC.

Gamaya

GEA Group Aktiengesellschaft

Farmers Edge Inc.

Gronetics

Order a free sample PDF of the Farm Management Software Market Intelligence Study, published by Grand View Research.

0 notes

Text

Thin Clients: Powering the Future of Virtual Workspaces

According to a comprehensive new market research report, the global thin client market was valued at USD 1.4 billion in 2022 and is projected to expand at a healthy compound annual growth rate (CAGR) of 4.2% from 2023 to 2031, reaching USD 2.1 billion by the end of 2031.

Market Overview Thin clients are minimalist computing terminals that rely on a centralized server or cloud infrastructure to execute applications, process data, and store information. In contrast to traditional PCs, thin clients minimize local processing power and storage, offering organizations a secure, scalable, and cost-effective alternative for deploying desktop virtualization solutions. Their deployment spans virtual desktop infrastructure (VDI), call centers, remote work environments, educational institutions, healthcare facilities, and financial services, where centralized management, standardized configurations, and data security are paramount.

Market Drivers & Trends Two primary forces are fueling thin client market growth:

Adoption of Cloud Computing: Enterprises are increasingly migrating to cloud-based platforms for email, storage, office software, and vertical-specific applications. Cloud-based VDI enables thin clients to access virtual desktops and applications on demand, delivering flexibility, rapid deployment, and operational efficiency. According to the European Commission, 42.5% of EU enterprises purchased cloud computing services in 2023, driving demand for thin client endpoints.

Demand for Centralized Management: Organizations seek comprehensive solutions for security management, patch deployment, asset tracking, and configuration control. Thin client architectures streamline these processes through a single pane of glass, reducing IT overhead and ensuring compliance with corporate policies.

Additional trends include:

Miniaturization and All-in-One Designs: Manufacturers are introducing compact, fanless thin profiles and all-in-one units to conserve space in modern offices.

Enhanced Security Features: Secure boot, multi-factor authentication, and hardware-based encryption are becoming standard to protect sensitive data in enterprise and government deployments.

Sustainability Initiatives: Energy-efficient hardware and reduced e-waste are driving preference for thin clients in organizations committed to green IT.

Latest Market Trends

Virtual Desktop Infrastructure (VDI) Acceleration: The shift toward hybrid and remote work models has reignited interest in VDI, with enterprises leveraging thin clients to deliver secure, high-performance virtual desktops to distributed workforces.

AI and Edge Computing Integration: Vendors are exploring AI-accelerated thin clients that offload inference workloads to edge servers, improving responsiveness for video analytics, telemedicine, and industrial automation.

Subscription-Based Models: Thin clients are increasingly offered as part of Device-as-a-Service (DaaS) and Desktop-as-a-Service (DaaS) bundles, simplifying procurement and enabling predictable OPEX budgeting.

Key Players and Industry Leaders The thin client arena is characterized by a mix of established IT hardware vendors and specialized endpoint solution providers. Leading players profiled in the market report include:

10ZiG

Acer Inc.

Advantech Co., Ltd.

Cisco Systems, Inc.

Dell Inc.

HP Development Company, L.P.

IGEL

NComputing Co. LTD

Praim SRL

Samsung

Each company is analyzed across parameters such as product portfolio, geographic footprint, recent product launches, strategic alliances, and financial performance.

Recent Developments

March 2023: Stratodesk announced certification of LG Business Solutions thin clients with NoTouch OS, enabling seamless deployment across private and public clouds, and giving IT teams enhanced flexibility for endpoint management.

August 2022: 10ZiG unveiled the 7500q thin client series featuring Intel quad-core processors, a 15.6-inch FHD display, up to 8 GB DDR4 RAM, multiple USB and HDMI interfaces, and up to 10 hours of battery life for mobile applications.

Access an overview of significant conclusions from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=40028

Market Opportunities and Challenges

Opportunities:

Emerging Economies: Rapid digital transformation in the Asia Pacific, Latin America, and Middle East & Africa presents substantial growth prospects for thin client adoption in sectors like education, public administration, and healthcare.

IoT Convergence: The proliferation of IoT endpoints creates demand for secure, manageable gateways, positioning thin clients as ideal enablers for smart manufacturing and logistics solutions.

Challenges:

Legacy Infrastructure Barriers: Organizations with entrenched PC deployments may resist migration to thin client architectures due to perceived risk and migration costs.

Network Dependence: Thin clients require reliable, high-bandwidth connectivity; inadequate network infrastructure in remote or underdeveloped regions can hamper deployment.

Future Outlook The thin client market is poised for steady growth through 2031, driven by digital workplace initiatives, sustainability mandates, and the need for resilient endpoint security. Innovations in edge computing, zero-trust security models, and AI-driven management tools will further enhance thin client value propositions.

Analyst Viewpoint "The convergence of cloud computing and the rising importance of data security in hybrid work environments underscore the strategic relevance of thin clients. Vendors that invest in advanced virtualization protocols, AI-based endpoint management, and energy-efficient designs are best positioned to capture market share over the next decade," says the lead analyst for enterprise infrastructure.

Market Segmentation

The report segments the thin client market as follows:

Component:

Hardware

Services

Deployment Mode:

Desktop-based

Mobile-based

Enterprise Size:

Small and Medium Enterprises (SMEs)

Large Enterprises

End-Use Vertical:

Banking, Financial Services and Insurance (BFSI)

Healthcare

Retail

Manufacturing

Government

IT & Telecom

Education

Transportation & Logistics

Others (Oil & Gas)

Regional Insights

North America accounted for the largest market share in 2022, driven by rapid adoption of cloud-based solutions, advanced IT infrastructures, and strong presence of key vendors. Europe follows closely, supported by digital transformation agendas in the UK, Germany, and France. The Asia Pacific is expected to register the highest CAGR from 2023 to 2031, fueled by industrial automation in China, government initiatives in India, and technology investments in Southeast Asia.

Why Buy This Report?

Gain data-driven insights on market size, forecast, and growth rate (CAGR 2023–2031).

Evaluate competitive landscape with detailed profiles of leading players.

Understand the impact of cloud migration, VDI acceleration, and security trends.

Identify emerging opportunities in new regions and verticals.

Leverage strategic recommendations from expert analysts to inform investment decisions.

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Farm Management Software Market 2030 - In-Depth Analysis on Size, Trends & Prominent Key Players

The global Farm Management Software (FMS) market was valued at USD 3.30 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 16.2% from 2023 to 2030. This significant growth can be attributed to the increasing adoption of cloud computing technologies for real-time farm data management, as well as the growing integration of Information Communication Technology (ICT), particularly technologies like the Internet of Things (IoT) and big data analytics in agriculture. These advancements help address a range of challenges that the agriculture industry faces, such as resource constraints (e.g., water, energy, labor shortages) and social issues (e.g., environmental concerns, animal welfare, and the use of fertilizers) that impact agricultural productivity.

Farm Management Software enables farmers to efficiently manage their operations by streamlining data collection, analysis, and decision-making processes. This approach helps in optimizing the use of resources and improving overall farm productivity. The integration of advanced technologies allows farmers to better monitor crops, manage soil health, and handle environmental challenges, ultimately improving the sustainability of agricultural practices.

The COVID-19 pandemic had a profound impact on the farm management software market. The pandemic led to significant disruptions in supply chains and posed operational challenges for the agriculture industry. In response, there was a marked increase in the demand for digital solutions. Farmers began relying more on digital tools to minimize physical interactions and optimize farm operations remotely. This surge in demand for data analytics and remote monitoring capabilities drove the adoption of farm management software. Moreover, precision agriculture gained momentum, as farmers increasingly relied on GPS-guided equipment, sensors, and other software-integrated tools to enhance resource utilization and improve operational efficiency.

Gather more insights about the market drivers, restrains and growth of the Farm Management Software Market

Regional Insights:

North America Farm Management Software Market Trends

In 2022, North America dominated the global farm management software market, accounting for 33.7% of the revenue share. The region is home to several prominent market players such as AgJunction LLC, Farmers Edge Inc., CropZilla Inc., and Deere & Company, which play key roles in the development and adoption of FMS. The market growth in North America is driven by the region's widespread adoption of precision agriculture practices, efficient resource management, and a strong focus on sustainability. Additionally, the growing emphasis on data-driven decision-making and ongoing advancements in agricultural technologies have bolstered the market's expansion in the region. These factors enable farmers in North America to optimize their operations, enhance productivity, and maintain a competitive edge in the agricultural landscape.

Asia Pacific Farm Management Software Market Trends

The Asia Pacific region is expected to witness the highest CAGR of 16.7% during the forecast period. Countries like China and Japan are at the forefront of this growth, with companies in the region increasingly investing in research and development (R&D) to introduce advanced drones aimed at improving agricultural productivity. Drones, integrated with farm management software, play a crucial role in enhancing productivity by enabling data collection and analysis. These drones, equipped with various sensors, capture valuable data about crop health, soil conditions, and field mapping, which is then processed by farm management software to provide actionable insights. Such advancements help farmers make informed decisions to optimize their operations.

Key market players in the region, such as Yamaha Motor Co., Ltd. (Japan) and DJI (China), are innovating by introducing drones with better sensors and imaging capabilities to enhance the quality of the data collected, thereby improving the efficiency of farm management.

Browse through Grand View Research's Category Next Generation Technologies Industry Research Reports.

The global mobile payment market size was valued at USD 88.50 billion in 2024 and is projected to grow at a CAGR of 38.0% from 2025 to 2030.

The global bank kiosk market size was valued at USD 19.57 billion in 2024 and is expected to grow at a CAGR of 16.1% from 2025 to 2030.

Key Companies & Market Share Insights:

The global Farm Management Software market is highly competitive, with numerous key players driving innovations and adopting strategies like partnerships and collaborations to strengthen their position in the market. One notable example is the partnership between Farmers Edge, Inc. and Google Cloud, announced in January 2021. This collaboration aims to enhance the company’s services by integrating advanced technologies such as artificial intelligence (AI), machine learning, and predictive analytics into its farm management platform. By leveraging these technologies, the company seeks to provide farmers with more accurate data insights, better predictive capabilities, and improved resource management, further driving the adoption of farm management software.

These companies are also focusing on the integration of new technologies like IoT, cloud computing, and data analytics to make farm operations more efficient, automated, and sustainable. As the demand for farm management software continues to grow, the competitive landscape is expected to intensify, with companies vying for market share by continuously innovating and offering advanced, user-friendly solutions.

Key Farm Management Software Companies:

Ag Leader Technology

AgJunction LLC

BouMatic

CropX, Inc.

CropZilla Inc.

DeLaval

DICKEY-john

Deere & Company

Corteva

CNH Industrial

Trimble Inc.

Climate LLC.

Gamaya

GEA Group Aktiengesellschaft

Farmers Edge Inc.

Gronetics